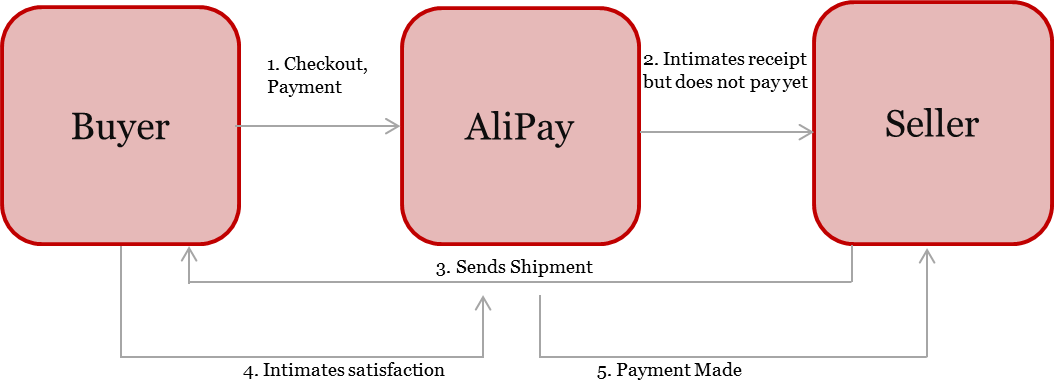

Businesses today have been extensively integrated with digitization, promising convergence of people and businesses, while disrupting existing business models. A new age of digital marketing has arrived where extensive campaigns are pushing new products through platforms such as websites, e-mails, apps and social networks. With over seven billion people and businesses, and a millions of technologies bringing a new world together, digital marketing plays a major role in empowering businesses with the much-needed edge to thrive with the competition.

Digital Business Development Path

Rapid change is fueling digital marketing. Within the last decade we have seen technology giants driving businesses such as Facebook and Twitter. Mobile marketing and advertising marketers have begun focusing on consistent and contextual without being interruptive. Change is the one thing that is constant, with changes being made faster than ever before. However, impact due to the change is highly dependent on it’s temporal context. For example, wearable technology like Google glass has gained a lot of news coverage when in fact, Steve Mann had already developed a similar device, ‘EyeTap digital Eye Glass’ in 1999. This is a prime example showcasing the importance of analyzing the visibility of a product with time for organizations to capitalize its technological and business resources to make the best marketing sense.

Hype Cycle

The Hype Cycle is a branded graphical tool developed and used by IT research and advisory firm Gartner for representing the maturity, adoption and social application of specific technologies (See Figure 1). The hype cycle map how technologies move through different phases of hype and indicate whether certain technologies and products are good for the company in short term and long term. Marketers need to understand how and when to derive value from a product and also when to dispose of it when new things come along.

Fig 1: Five Phases of the Hype Cycle (source: Gartner)

What’s new in 2014?

Marketing Talent Communities: Marketplaces have come up that support organizations and marketers to find and hire qualified freelance talent on-demand. A lot of time is saved in the process of recruitment of a variety of qualified writers, designers, strategists, data-analysts etc. Bloomberg Institute is one such example which financial employers approach to hire talented college students through a normalized screening test called the Bloomberg Aptitude Test.

Marketing Technology Integrators: The scope of digital marketing has expanded broadly. Digital marketers can’t claim to address the digital marketing needs solely through offering new Web Content and Experience Management or Portal platforms. As a marketer, the time and attention required to solving technological solutions takes time away from their focus on target customer. Thus, marketing organizations are hiring services and products that design and implement software and increasingly integration-oriented implementation data solutions.

Transactional Ads: This is an example trying to connect marketing with productivity and conversion. Online ad units that are activated by gestures, present a secure transaction or coupon. This reduces the time consumption of the viewer by enabling a person to request information or to buy the advertised product without leaving the webpage on which the ad appears. If old companies can figure out a way to associate more with transactions, they can boost their chance of surviving in the online market. [3]

Quantified self: It is a movement to incorporate technology into data acquisition aspects of a person’s daily life in terms of inputs, states and performance. Applications or services on mobiles and wearable technology that provide self-tracking analytics contribute to self-knowledge through self-tracking with technology. Biometrics have been identified that people never knew existed making data collection cheaper and more convenient than ever before. Recently, companies like Google and Zomato have begun to use location data of a user’s phone to recommend suggestions to buy things based on the proximity to various shopping outlets.

Social co-browsing: Collaboratively sharing of the web space with one or more parties from a social network, regardless of the physical locations of the partners. In real-time, multi-user experience isn’t just slapped on top of an application, it’s directly built into the core experience. Companies would have to redesign their user experience to support social co-browsing so as to provide a natural extension of for users to communicate and interact to enrich their real-time, collaborative experience. [4]

Future Implications

Most of the technologies at the peak of their hype cycles today, will plateau in terms of productivity within the next two years. The window to gain competitive advantage in this fast-paced environment is limited. Thus companies must adapt themselves for speed, agility and rapid customer response.

Content marketing can be very resource intensive. Organization should use marketing talent communities and agencies as an escape valve for demand as a way to scale elastically as demand comes online. The in-source and outsourced roles must be carefully mixed together in order to optimize productivity. Organizations should appoint strong leadership to ensure the success of their elaborate content marketing strategy.

Common view of digital-savvy customers should be kept in focus to ensure tight coordination of marketing activities in sync with the changing customer needs and reactions. Emerging architectures of digital marketing hubs should be carefully reviewed periodically to best utilize resources for most productive outcome.

With increase in social-marketing hype, the social marketing objects should be tied to the corporate vision of the companies. Analysis of how each social marketing activity will support that goal and provide a high return of investment. Gain from adapting to emergent technologies can lead to savings on media from improved efficiency or lift in sales from improved effectiveness of a company’s budget.

B2B management investments should be made into multi-channel, taking advantage of accessible areas in data mining, segmentation and behavioral analytics. Useful analytic results should be incorporated to the marketing strategy to further boost performance.

Criticism about Hype Cycle

Several disadvantages of Hype Cycle have been brought to light. Firstly, it is very difficult to objectively estimate the current location of a technology in its hype cycle. Secondly, terms such as ‘disillusionment’ and ‘enlightenment’ are misleading for people as they give a wrong idea about how exactly and to what extent a technology can be used for an organization. Also, there is no mention of how a technology transitions between phases and what all factors influence the shift. Lastly, several technologies are heavily correlated in terms of advancement through the different phases. The hype cycle does explain the cause-effect relationships between technologies and their impact on acceleration of technology progress and generation of excessive hype for a product.

References:

http://www.gartner.com/newsroom/id/2819918

http://www.theregister.co.uk/2013/03/02/steve_mann_on_google_glass/

http://techcrunch.com/2010/03/07/the-rise-of-transactional-advertising/

https://goinstant.com/blog/collaborative-customer-interfaces-and-social-cobrowsing